Although a lot of water has flowed under the bridge since the roundtable with Jürgen Habermas, Joschka Fischer, Henrik Enderlein and Christian Kallies held in April 2011, they identified some key political factors behind the euro crisis, as subsequent events have amply confirmed.

Firstly, there are the design flaws in the monetary union. As Henrik Enderlein pointed out, the actual EMU was an unstable compromise between two coherent views – the German position that currency union should be postponed until a great deal of integration and economic convergence had already been achieved and the French view that immediate monetary union should be accompanied by the establishment of a European economic government. The unworkable outcome was immediate union without complementary institutions.

Secondly, the roundtable agreed that there is no way backwards out of the crisis. As Habermas said, “we are faced with a choice between jeopardizing the degree of monetary union that we have already reached or, at the very least, setting out the institutional preconditions for closer cooperation between member states”. These German discussants all insisted that Germany in particular had gained a lot from the euro and would be a big loser if it failed.

A third point concerned the failure of German leadership in the EU. Habermas’ speech traced the weak and reluctant response to the developing crisis to a deterioration of political conditions in Germany. On the one hand there had been a change in attitudes after German unification towards a narrower and more self-absorbed view of Germany’s place in Europe and the world. On the other, in Germany as elsewhere, the quality of political debate had been impaired by opinion-poll led opportunism in the political class, by the trivial, short-term focus of the media and by the merging of the media and political elites into a self-interested grouping no longer capable of influencing public opinion in a constructive way. To reflect the very apt coinage used by Habermas, one might say that German political culture had been Berlusconified.

The present contribution considers recent economic developments in more detail. It aims, with one exception, rather to endorse and illustrate the positions of the roundtable participants than to contest them. It looks at three issues: the unfolding sovereign debt crisis which has found eurozone leaders in general and the Merkel government in particular repeatedly overtaken by events; the authoritarian and repressive “Pact for the Euro”, which has now become the central integration strategy of the EU; and, finally, the role of Germany in the crisis. On this last issue there is a certain difference with the roundtable commentators, because I suggest that the present failure of the German government to meet its international economic responsibilities has important precedents twenty and thirty years ago.

The unfolding crisis

To follow developments in the eurozone through 2011 has been to watch a car crash in slow motion. An English proverb traces the downfall of a kingdom to the lack of a horseshoe nail. The GDP of Ireland is euro 156 billion. Assistance to Ireland of, say, 10 per cent of its GDP would have been a bagatelle for the strongest and largest economies of the EU, and even within the capacity of the EU itself, although its budget (euro 140 billion in 2011) is only some 1.2 per cent of EU GDP and is generally recognised to have no macroeconomic significance.

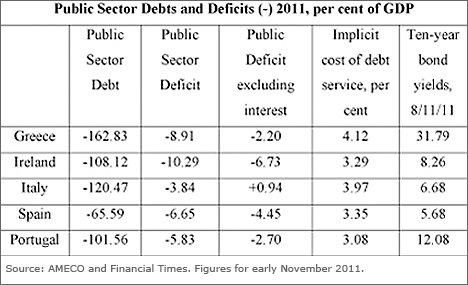

The GDP of Italy is euro 1568 billion, just over ten times as much. The outstanding debt of the Italian state approaches euro 2 trillion. If the claims corresponding to that debt turn toxic then the financial disruption which follows will be of the same order of magnitude as after the failure of Lehman Brothers in 2008. Even a rise of five percentage points in the cost of debt service – now more likely than not – makes for an enormous gap in Italian public finance. Yet decisive assistance for Ireland and Greece (GDP euro 217 billion in 2011) would have prevented contagion to Italy.

This section briefly reviews responses to the sovereign debt crisis. The first four measures have been put into practice. They fail because they are insufficient to resolve the problem. The following three could work but are blocked by the absence of political agreement and especially by German refusal.

Rescue techniques which have been at least partially implemented include:

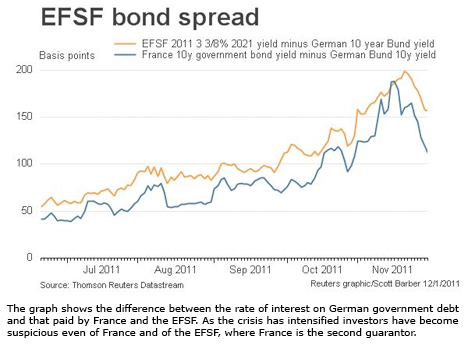

1. Emergency credits to governments in difficulties, extended bilaterally or through the IMF or the EFSF, to be replaced in 2013 by the ESM. Because the first Greek bail-out was arranged, by the Commission and the IMF, prior to the establishment of the EFSF, and because the second had not yet been paid at the time of writing, by late October 2011 the EFSF had only made three relatively small loans totalling euro 9.5 billion – one to Ireland and two to Portugal at interest rates around 6 per cent. It borrows at rates substantially below that and up to late October had issued bonds to the tune of euro 13 billion. However, as the eurozone crisis has intensified, a certain risk premium has emerged even for the AAA rated EFSF (as for AAA rated France).

The EFSF was able to borrow cheaply because it has guarantees of its liabilities from the member states. However, these are for limited sums. The guarantees, increased in July 2011, total euro 780 billion, with the main ones being euro 211 billion by Germany, euro 158 billion by France, euro 139 billion by Italy euro 92 billion by Spain and euro 44 billion by the Netherlands.

The agreement reached by Eurozone leaders on 27 October will see an euro 8 billion tranche of a previous EU-IMF loan released and a new loan to Greece, this time from the EFSF, of euro 130 billion. However euro 30 billion of this is intended to go as a “sweetener” to investors holding Greek bonds to persuade them to accept a haircut. It was also agreed that the facility should be leveraged in the following sense: instead of lending directly to governments or purchasing government debt, the EFSF will be able to offer partial insurance of new issues of government bonds on the market. It is hoped that this will increase the funds which can be made available to governments with financing problems, member states having to increase the amount of EFSF borrowing they are prepared to guarantee. It seems that the German government in particular has refused to increase its guarantee.

The limitations of the EFSF are many. Firstly, the fact that its credit-worthiness is seen by investors as similar to that of France rather than that of Germany shows that its own position could become fragile. In particular, if support is required for Spain or Italy then huge new commitments from guarantor states would be needed at the same time, since otherwise the new EFSF borrowing would not be guaranteed. The leveraging of EFSF assets will tend to call its liabilities into question if Germany does not increase its guarantees.

The limited power of the EFSF was demonstrated when it raised the relatively small amount of euro 3 billion – destined for Ireland – on 7 November 2011; it had to offer yields substantially higher than on a previous issue in June. A week later the head of the EFSF, Klaus Regling, recognised that it might not be possible to increase the fund to euro 1,000 billion as the eurozone countries wished. This is because of market upheaval – but, presumably, the EFSF was supposed to prevent such upheavals, rather than succumb to them. An EFSF document describes its current objective – set by eurozone heads of state and government – as “enlarging the capacity of the EFSF without increasing the euro-area Member States’ guarantee commitments underpinning the EFSF”. But that is exactly the point: the refusal to increase the guarantees – specifically to engage the full faith and credit of the German state – means that investors’ mistrust of highly indebted sovereign borrowers extends to the EFSF itself.

Secondly, the loans extended by the ESFS are at relatively high rates of interest and thus do not reduce the burden of debt service for the loan recipients as much as possible. Likewise, the conditions imposed on the recipients may prove to be counter-productive: this certainly seems to be the case in Greece, where GDP has fallen for four years in a row. Finally, of course, the whole exercise is aimed at providing liquidity rather than dealing with insolvency – debt rollovers as such do not remove an excess of liabilities over assets.

2. Haircuts for the holders of sovereign debt seem to address the solvency issue directly. A first exercise of this kind took place in July 2011. It was voluntary on the part of the bondholders, who were induced to swap their existing Greek paper for much longer dated bonds with a somewhat lower face value. The terms were so generous to investors that they hardly reduced the burden of Greek debt, especially when it is realized that Greek bonds were already significantly discounted on the market, making it possible to buy them back well below their face value.

Pressure to avoid significant losses for investors came obviously from the investors themselves, from the ECB, whose normal functioning presupposes the validity of eurozone government debt, and from the issuers of credit default swaps on Greek paper, who would have to pay out if a default was declared.

A more serious write-down was included in the October 27 agreement: a 50 per cent reduction in the face value of Greek bonds with the aim of cutting the indebtedness of the Greek government to 120 per cent of GDP by 2020. However, the details of the write-down remain to be negotiated with the Institute of International Finance, which represents many of the biggest investors. It seems that there will still be an attempt to reach a voluntary agreement and avoid an open default.

In principle, the problem of debts which cannot be repaid should be resolved by the cancellation of government debt against assets, most obviously against the actual bonds which that government has issued. Therefore a haircut at least goes further than simple “bail-outs” which rearrange, without reducing, state indebtedness. There are two main objections to the haircut which was announced, without many details, on 27 October 2011, although they point in different directions – one for a bigger, one for a more moderate write-down. On the one hand it seems very likely that the debt relief provided to the Greek state will be insufficient: the remaining debt will prevent the launch of measures to support production and productivity. On the other, the losses imposed on creditors may directly weaken the banks and other financial institutions involved, or lead to a self-fulfilling expectation of further losses from defaults by other states.

The Greek banking sector is a special case – it holds some euro 50 billion of Greek government paper; any substantial write-down would necessitate comprehensive refinancing. But exposures are high elsewhere and thus the haircut could lead to two processes of contagion – from Greece to other states and from the first affected banks to others. Thus the haircut proposal agreed, at least in principle, is necessarily associated with:

3. Recapitalisation of the banks to the tune of euro 106 billion. This is part of the October package, largely to immunize them against the planned write-down of Greek debt. The Greek banks themselves are the most exposed and the EFSF loan to the Greek government includes some euro 20-30 billion intended to strengthen their position. It is not clear that this is enough because the Greek banks have other doubtful loans on their books and are also facing a run-off of deposits as their customers protect themselves against a possible exit from the euro. Elsewhere it does not seem that the sum involved will greatly embarrass the banks, as they will be able to raise it through retained profits and without having to sell bank shares at what are currently very low prices. Banks in Spain, Italy, France and Portugal have the biggest targets for extra capital – of euro 26.2 billion, euro 14.8 billion, euro 8.8 billion and euro 7.8 billion respectively. German banks (Deutsche Bank and Commerzbank are affected) only have to find euro 5.2 billion. The assumption behind this measure is that the banks will not have to deal with further write-downs or defaults on sovereign debt, and, in particular, that contagion to Spain or Italy will not occur.

Of course the environment in which the banks function is strongly influenced by:

4. Accommodating actions by the ECB. Like most central banks, the ECB cut interest rates in the financial crisis and subsequent recession, although not as much as the Federal Reserve or the Bank of England. Two interest rate rises were made when it seemed that the eurozone economy was recovering. In an early decision under the new ECB president, Mario Draghi, one of these has since been reversed. The generally low rates at which commercial banks can borrow are being passed on to their depositors but not to their debtors – thus banks are being recapitalised by their customers. The ECB’s mandate calls for it to support EU economic policy when this can be done without prejudice to price stability. Since the recession itself has tended to keep prices in check this creates a certain room for manoeuvre.

There is a grey area between the supply of liquidity and support for governments under financial pressure. Direct finance of governments by the ECB – in “primary” debt markets – is illegitimate, but the ECB must have at least some presence in secondary markets because it often takes government bonds as collateral in its lending to commercial banks. (In fact, the ECB also accepts a very wide range of other securities in such lending.) Until the financial crisis, the stability of sovereign debt markets and the rough equivalence of paper issued by the different member states was a premise in ECB operations and therefore the need to facilitate these operations has justified a somewhat more active role for the ECB in security markets.

Paul De Grauwe points out that after the eruption of the Greek crisis in May 2010 the ECB became more restrictive and started to reduce its purchase of government bonds. However this reversal now seems itself to have been reversed. There have been two main programmes for the purchase of securities – one aimed at “covered bonds”, essentially asset-backed securities issued by the private sector of the kind which was most impaired by the sub-prime crisis, and the other at government bonds issued by the more troubled countries. When there seemed to be a certain stabilization of the situation, the programme was suspended between April and August 2011. It was then resumed “after the announcement of new fiscal and structural policy measures by the Italian and Spanish governments.” Clearly the ECB seeks to make this support conditional on restrictive measures in the countries concerned.

The purchase of government bonds and other securities by the ECB is on roughly the same scale as similar purchases by the Federal Reserve System in the US. On the other hand, the Fed was not faced with potential defaults on the scale of those now menacing the eurozone. The ECB has leaned against the wind in the bond markets. But its actions have been too little and too late to prevent either a tightening of the financial pressures on the most vulnerable states or the spread of these pressures to states which were previously unaffected.

Measures which might prove effective but which are at present politically blocked are of two kinds:

5. Eurobonds. This term denotes the substitution of the EU, or an institution established by the EU, for the impaired borrowers in Greece, Portugal and so on. Since the financial crisis of 2008-9, borrowers perceived as risk-free have enjoyed very low interest rates; if rates could be reduced for the eurozone as a whole, then debt service would be much more manageable.

The table indicates that, so far, only a relatively small part of the debt of the peripheral countries has to be serviced at current bond market yields because most of it was issued at much lower rates. The new higher rates become payable as governments roll over their debts. But a vicious cycle now appears. The very fact that default is now more likely makes investors charge a higher interest rate; on the other hand, the fact that governments have to pay higher rates makes default more probable. Eventually governments cannot borrow from the markets at all – this is already, in effect, the position of Greece. On the other hand, if the effective interest rates were lowered to those prevailing in Germany (1.79 per cent), or even the heavily indebted UK (2.26 per cent), there would be a substantial reduction in the financial pressure in all countries except Spain, where indebtedness is relatively low.

The present highly cautious behaviour of investors, although it is disastrous for the peripheral counties, is a windfall for governments able to issue trustworthy debt, because investors will settle for very low returns rather than risk their capital in very volatile financial markets. Given inflationary prospects, the real interest rates being paid by the governments of Britain, the US and Germany are negative. The Eurobond proposal amounts to extending the benefit of this very cheap credit to the governments in difficulties. Such a measure might not suffice – debt forgiveness might still be needed to stabilise the situation, especially in Greece. But it would move all the economies involved a long way towards stability at little or no cost to the guarantors. The solution fails because the EU as a whole is not prepared to undertake such a course of action, and because Germany refuses to add its full guarantee to the already existing eurozone body, the EFSF. Without such an assumption of debt by the EU as a whole, or by the German government, investors will not regard the eurobonds as essentially safer than the impaired debt of the weaker member states. But if a collective bond issue is ruled out then the only immediate barrier against the contagion of crisis is…

6. The “wall of money”. This expression originally signified the obstacle to social reform which moneyed interests constituted in 1930s France. Today it has been given a completely different meaning: the strategy, available to a central bank of simply smothering financial tensions with super-abundant credit. If crisis-struck governments could borrow unlimited sums from the ECB both to service existing debt and to cover current deficits then they would be in a position to deal with both debt and deficit by the most effective method of expanding output and income. Debt “sustainability” depends on the interaction of growth and interest rates; when the latter are close to zero and the former around two or three percent, a few years will transform the balance sheet.

Paul De Grauwe argues for this policy: “To prevent further drops in government bond prices, the bank should announce that it is ready to intervene in the market. The ECB is the only institution capable of doing this because it can create money without limit. In announcing its unconditional commitment, the bank would stop the spiral of decline. And when investors were convinced of the resolve of the ECB, they would stop selling sovereign bonds because they would trust that a floor had been put on their prices. The beauty of this outcome would be that the ECB would not have to buy government bonds any more.”

Martin Wolf takes the same position. He urges Mario Draghi, incoming president of the ECB to take the expansionist path:

“Could Italy survive by slashing spending? No. If the country tried to redeem its debt out of revenue, it would need to slash spending by far more than a fifth of GDP, overnight, since the very attempt would tip the country into a depression. No sane creditor imagines that a country could roll over its debt in this situation. Government debt markets are lifted by their own bootstraps: the willingness to lend depends on the perceived willingness of others to do so, now and in future. Such markets are exposed to self-fulfilling runs and so need a credible buyer of last resort: the central bank.”

Both De Grauwe and Wolf dismiss the risk of inflation: on the one hand the lack of demand in the eurozone economy is holding back prices; on the other the investors who are selling Italian or Spanish bonds are not looking to purchase different risky assets; they want money as a store of value. In principle there are moral hazard dangers in bailing out governments but these are no different from those already faced in bailing out banks.

Willem Buiter, while deploring this use of the central bank, also sees large-scale ECB purchases of government bonds as necessitated by the failure to reach a politically agreed solution: “The choice, sometime in 2012 or, at the latest, 2013, will be between a collapse of the euro area and large-scale quasi-fiscal abuse of the ECB. Finally, because neither restructuring of insolvent sovereigns, nor recapitalisation of zombie banks, nor ring-fencing of those sovereigns that are mostly likely solvent but vulnerable to illiquidity ambushes have been addressed decisively and completely, tight financial conditions and intensifying fiscal austerity will contribute to a European recession in 2012 and possibly beyond.” German opposition to the ECB acting as a lender of last resort to governments was signalled, within days of Draghi taking office, by the president of the Bundesbank.

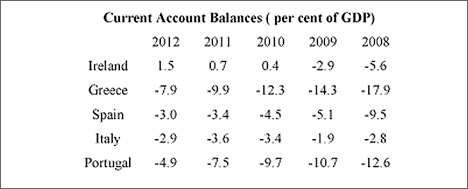

7. Fiscal Union is the final measure to be considered. However, it seems more of a structure for the medium term avoidance of new crises than an immediate remedy for the problems of state indebtedness. Agreed fiscal transfers would support the kind of collective refinancing discussed under the “eurobond” heading above. At present, most commentators suggest, there is little prospect of the Treaty amendments that might be necessary to establish a “solidarity or transfer union”, in the words of Joschka Fischer. The current account deficits of the peripheral countries have improved recently but this is simply because deflation and recession have restricted imports. If these economies started to grow they would soon run into an acute balance of payments constraints.

To avoid this problem there would either have to be a very big expansion in Germany and other Northern economies (to encourage imports from the peripheral economies) with a big rise in German wages (to make Germany less competitive relative to those economies), or fiscal transfers from North to South to pay for their increased imports. But, as so often in the EU, the rationality and necessity of a reform is not enough to bring it about. The next section will argue that the way in which EU and national authorities have decided to push integration forward, without significant transfers, threatens democracy and the social models in the weaker economies.

Towards the surveillance union

EU leaders realise that institutional reforms are needed in the eurozone. The Stability Pact, intended to guarantee budgetary discipline and thus economic stability, failed in two ways: some countries, such as Spain and Ireland, suffered enormous crises in spite of their obeying the Stability Pact rules; others, such as Greece, clearly violated the rules continuously. However the response adopted by the EU ignores the fact that only these malfunctions – only the build-up of imbalances – permitted the eurozone to achieve even the mediocre employment performance that it recorded.

In several ways, EU authorities are preparing a post-crisis regime which will install a comprehensive tutelage over the weaker economies. Some of this is already apparent in the conditions imposed on crisis-struck countries, in particular Greece. In return for EFSF finance, Greece is required to make big changes which would normally depend on internal debate – such as privatisations and alterations to pension arrangements. A particularly worrying demand from the creditor authorities is the decentralisation of collective bargaining – an attempt to dismantle a social model which European law requires the EU to respect.

As Habermas puts it, governments will be inspected every year to see whether “the level of debt, labour market deregulation, the system of social security, the health care system, wages in the public sector, the wage share, the rate of corporation tax and much more correspond to the reckoning of the Council.” He could have pointed out that such surveillance will be of the weak by the strong.

The rules of the “Growth and Stability Pact”, supposed to govern the budgetary policies of all EU members and to be obligatory for members of the eurozone, were based on the fallacious notion that, provided public sector deficits were limited, market forces would ensure a balanced development of the economy. In reality there developed very large current account deficits across the periphery which became impossible to finance after the crisis of 2008.

The financial crisis of 2008, provoking a rapid decline in private sector expenditures, necessitated substantial public sector injections around the world. The Commission had to recognise that much wider public sector deficits were needed temporarily, but already by 2009 it was demanding an early “exit” from these more supportive budgetary policies. At the same time it made proposals to make the Stability Pact rules on public sector borrowing and debt much more restrictive and to introduce new rules on macroeconomic “imbalances”.

The official rationale for these changes is couched in terms of both “coordination” and “surveillance”. But they do nothing to promote coordination. Genuine coordination would require firstly the specification of an overall macro policy for the eurozone and then the specification of differentiated national policies compatible with the overall macro stance. There is nothing of this in the proposed amendments. In reality, the only focus of these measures is on the surveillance of individual member states and, although this is not stated, the concern is only with the weaker member states to whose “indiscipline” the current crisis is attributed. Thus the whole package neglects the central problem of coordination – the huge imbalances in current accounts.

The reform comprises six pieces of legislation, which have, in autumn 2011, passed through the European Parliament with very few changes. The first four tighten the requirements of the existing stability pact and its enforcement through the “excessive deficit procedure”. The other two introduce an “excessive imbalance procedure” which introduces similar legal constraints on other aspects of macroeconomic policy; they are obviously inspired by the fact that in Ireland and Spain the crisis had nothing to do with public sector deficits but relates to capital inflows into the private sector. A brief description of this legislation is as follows:

Tightening the Stability Pact:

1. New definitions of the stability pact rules emphasise “excessive” levels of public debt as well as well as annual deficits; “discretionary” measures have to be taken to correct both and the speed of correction is specified. The only permitted exceptions have a strongly deregulatory character – a member state may run deficits to introduce a funded pension scheme, but not, for example, to finance a social housing programme.

2. Stronger surveillance is to take place through the annual submission of stability programmes (including “structural reforms”) which must embody a medium-term budgetary objective to permit the Council to verify “prudent” fiscal policies. Even countries within the prescribed limits for debt and borrowing must not increase public expenditure faster than GDP (thus any move by other countries towards Scandinavian social models becomes illegal).

3. Reinforced penalties involve first compulsory deposits and then fines for eurozone members. Sanctions are to become more automatic since at many stages of the “excessive deficit procedure” a qualified majority in the Council will be needed to block penalties rather than to impose them, and therefore it will be harder for countries subject to the procedure to gather enough political support to escape the penalties.

4. Member states must establish a satisfactory budgetary framework. This covers accounting systems, statistics, fiscal relations with regional and local government, forecasting practices (although the Commission’s own forecasting is less than impressive), budgetary procedures and “fiscal rules”. It is strongly recommended that the latter involve numerical limits (i.e. ceilings on public spending and on government borrowing) in spite of the repeated difficulties that such rules provoke, most recently with public finance in the US today (and no doubt Germany in the near future).

The Excessive Imbalance Procedure:

5. A scoreboard comprising “a limited number of economic and financial

indicators” is to be established. “Indicative” thresholds will be set for these; if they are crossed investigative procedures may be launched; however there will not be an automatic alert; “economic judgement should ensure that all pieces of information, whether from the scoreboard or not, are put in perspective and become part of a comprehensive analysis”; this will identify member states to be subject to an “in-depth” review. Such as review will involve “enhanced surveillance missions” and additional reporting by the member state concerned.

6. Penalties do not follow right away. When excessive imbalances are definitely identified, “recommendations” will be made to the member state. Its response should be timely and should use “all available policy instruments”, including fiscal and wage policies, labour markets, product and services markets and financial sector regulation. Eventually, however, if the response proves inadequate, sanctions – compulsory deposits and fines – will be imposed. Equity in penalties is to be assured by expressing these as a percentage of the GDP of the recalcitrant state.

There is, of course, something absurd, even ridiculous, about this attempt to construct a juridical framework for macroeconomics, as anyone remotely familiar with that discipline will recognise. But the project is also sinister: it threatens to subject economically weaker members – and those alone – to a comprehensive tutelage involving every aspect of public policy. It is clear that the main indicators used will reflect so-called problems of “competitiveness”. Criticism in the European Parliament and by some EU governments has led to the removal of explicit reference to wages in the legislation (early drafts from the Commission referred explicitly to excessive wage costs as a key “imbalance” in the weaker economies). But the wage levels and social models of the weaker states remain the targets of this project.

Many types of “imbalance” will be outside the scope of the new procedures. These include: the coexistence of immense private fortunes with public sectors crippled by debt; the failure of wage growth in the EU to match productivity growth over three decades; the remuneration of financial and corporate leaderships out of all proportion to typical incomes.

The package is embedded in a reinforced set of administrative procedures known as the “European semester”, which will take place in the first half of each year and lead to the definition of two sets of policies, one concerned with macroeconomic policy (the “stability programmes”) and the other (the “national reform programmes”) concerned with “structural reforms”, in the Commission’s usual sense of reduced protection for employees, privatisations and deregulation of business. The first such exercise, which took place in 2011, indicates what is to be expected from these procedures: neither Commission recommendations for Germany nor Germany’s own programmes recognised any problem with its huge surplus of exports over imports. This surplus results from German policies to keep down spending in Germany and to make higher exports the main way in which the German economy grows. But export pressure from Germany necessarily means big trade deficits in the weaker economies; it is their deficits which are the counterpart of the German surplus. The entire process focuses on further fiscal consolidation, labour market “reforms,” and supply-side measures supposedly to promote growth by “large price and cost adjustments” in the weaker economies – in other words, by deflation.

The consequences of this stance can be anticipated by anyone sceptical about the notion of growth-promoting deflation. By September, the Commission was compelled to revise downwards its already low predictions for growth in 2011 and 2012. It declared that “the downward revisions concern all the Member States under review, suggesting both a common factor and a re-coupling of growth dynamics”.

What is being referred to here? One “common factor” is of course the constant pressure for restrictive policies (lower public spending and higher taxation) coming from the Commission and from political leaderships in most member states. Another is the looming financial crisis stemming from repeated failures to resolve the crisis in Greece. The rediscovery of “re-coupled dynamics”, on the other hand, points to genuine coordination problems neglected by those same leaderships who have preferred to attempt a virtually colonial subordination of the weakest member countries. This is the way the eurozone will continue if and when the crisis is surmounted – it makes one doubt whether there is any value in preserving the monetary union.

The continuity of German policy

Both Habermas and Fischer very correctly point out that in Germany there has been a certain loss of enthusiasm for the European project. This perhaps helps to explain the hesitancy of the German response to the deepening eurozone crisis. However, it is certainly not the case that the attitude of Germany’s leaders to international economic problems has always been constructive and cooperative. On the contrary, Germany has got form in the dogmatic destruction of international systems.

The case of the European Monetary System (EMS) is well known. The EMS, established in 1979, involved fixed exchange rates among European countries. It failed in 1992-93 because, with fixed exchange rates, interest rates had to move roughly in parallel and German monetary policy, after reunification, involved very high interest rates. As De Grauwe pointed out, the Bundesbank squeezed long and hard against inflation which never reached 5 per cent. Germany’s partners in the EMS could not live with interest rates pushed to 10 per cent. The German authorities argued that they would be prepared to moderate interest rates if the other countries devalued and thus cut Germany’s import costs and worked to further disinflate the German economy – hardly the most critical policy objective of the time. On the other hand, Germany’s partners were using their D-mark pegs as anchors for their own disinflationary strategies – devaluations meant for them the complete failure of their economic strategies. It is most improbable that the benefits to Germany, if any, from this sabotage of the EMS matched the losses imposed on their partners. The episode can be summed up by saying that the other EMS members wanted Germany to act as a leader and to manage the overall reduction of inflation across Europe but that Germany refused to play this role.

Less well-known is the role of Germany, thirteen years earlier, in the most important economic turning point since 1945 – the Volcker shock. At the end of 1979, faced with runaway inflation and a rapid depreciation of the dollar, the Federal Reserve moved decisively towards monetary restriction – pushing interest rates up above inflation rates at the cost of two sharp recessions in the US itself. The impact elsewhere changed the world: developing countries were plunged into a debt crisis more than a decade long; Keynesian policies in western Europe became almost impossible to finance so that Duménil and Lévy could characterise the Volcker shock as a “neo-liberal coup”.

Clearly this was fundamentally a US decision. But the German authorities were complicit. In the autumn of 1979, as the dollar fell like a stone on the foreign exchanges, Volcker visited Germany to ask for support from the Bundesbank. Chancellor Helmut Schmidt and Bundesbank president Otmar Emminger turned him down flat. Emminger records with astonishing complacency that he told Volcker to get the US money stock under control and that as Volcker left he conceded this: “you’re right – the really decisive factor is the money stock”. It would be hard to find a better example of sowing the wind, and Germany itself was certainly not spared by the whirlwind that followed.

These precedents certainly do not reduce the responsibility of the present German leadership, whose pusillanimity has brought the global economy to the brink of collapse. But, for whatever reason, Germany has a long record of dogmatic and dysfunctional decisions on macroeconomic questions. This record does not encourage optimism as the eurozone approaches the abyss.