From the early 1980s, the British economy became the subject of an allembracing economic experiment. At the heart of this economic leap-in-thedark was a switch in philosophy from the “managed capitalism” of the postwar era to one of “market capitalism”. The former commitments to full employment, progressive taxation and inclusive welfare were dropped. Most elements of the postwar settlement – and its belief in economic fine-tuning, greater equality and a strong state – were discarded. Regulations were swept away and corporate and top income tax rates axed. Markets were given more freedom. Although this shift to market capitalism was applied most strongly in the United Kingdom and the United States, weaker versions were eventually introduced across much of the rich world.

The experiment came with big promises. The medicine of the market, it was claimed, would overturn the failings of post-war welfare capitalism. The “supplyside” measures – weakening the power of collective bargaining, reducing taxes at the top and giving business and finance more freedom – would unleash a new era of enterprise, entrepreneurialism and dynamism. The elevation of finance to a more central place in the economy would lower financial risk. Freeing up markets would raise Britain’s growth rate, create more jobs and businesses and bring greater prosperity for all. Countries like the United States and the UK which adopted extensive deregulation would experience less economic turbulence.

The new theories on the virtues of freer markets were developed from the 1960s, mainly by a group of American economists, from Milton Friedman to Robert Lucas, many of whom were based or had trained at the University of Chicago. Central to the new philosophy was a belief in efficient and self-regulating markets. Using the tools of advanced mathematics, these prophets of the market school constructed highly sophisticated and rigorously tested economic models that claimed to demonstrate that free and flexible financial and labour markets deliver greatly superior economic outcomes – on employment, productivity and growth – than regulated ones, and that government failure was much more likely than market failure. They also welcomed the personal wealth booms that accompanied the birth of the free-market era. Greater inequality was interpreted as a healthy sign that markets were working. According to their economic models, markets were self-regulating, economic shocks would quickly be reversed, while any tendency to imbalance would be quickly corrected provided markets were free to adjust.

So what about the record of the thirty-year long era of market economics? Has the market experiment delivered on its claims? Have Britain and the other countries adopting the market model, such as the United States, enjoyed greater economic prosperity and stability than in the more interventionist post-war era?

For a decade from the mid-to-late 1990s, it seemed that the new prophets might be right. After serious birth pangs in the 1980s and early 1990s – when restrictive macroeconomic policies blunted growth rates – the more open and globalised world economy entered a period of sustained growth. Although this upward path faltered slightly in 2000 and 2001 with the bursting of the new economy bubble, average growth rates across the world and the richer nations were higher between 1997 and 2007 than they had been in the period 1981-1996. Growth in both the UK and the US – an annual average of 3.0 and 3.3 per cent respectively in the decade to 2007 – outstripped that of the other G7 nations less wedded to markets (Japan, Germany, France, Italy and Canada), which averaged between them only 2.4 per cent. These figures lent some support to the market school. But we now know that this apparently promising economic performance, a solid improvement compared with the 1980s and early 1990s, was an illusion. One study, by the City brokerage firm Tullett Prebon has estimated that, after stripping out what they call “the Brown bubble borrowing”, the UK’s real growth from 2000 to 2008 was half ist headline rate. Half the much vaunted growth over this period was artificial. Moreover, while the contribution to the economy made by financial services (the “bubble effect”) more than doubled over this period, manufacturing shrank by a quarter and mining by more than a quarter. During the UK’s post-millennium boom years, the money and productive sectors of the economy were moving in opposite directions.

There was no economic miracle. Freer markets, and the escalating rewards at the top to which they gave rise, failed to deliver the sustained improvement in economic performance that had been promised. For their advocates, the new economic orthodoxy was to be judged above all on its impact on the real economy, on whether it delivered more productive, efficient and innovative economies. Yet the evidence is that market capitalism has been weaker on most key measures of economic performance than the period of managed capitalism. This is clear from dividing the post-war era into two distinct periods. The first – the 23-year period of “managed capitalism” – dates from 1950 to 1973, the year of the first OPEC oil shock and the one which perhaps best marks the end of the post-war boom. The second period – the 29 years of “market capitalism” – covers the period from 1980 to 2009, beginning with the first full year of the new economic experiment.

Of course, there was no shortage of problems facing the UK economy in the 1950s and 1960s, from periodic sterling crises and an outdated industrial structure to falling competitiveness and deteriorating industrial relations. But, on only one count – curbing inflation – can the post-1980 era be judged a clear success. Inflation rates tailed off during the 1980s and have remained lower ever since. On all other counts, the economic record of market capitalism has been inferior to that of managed capitalism. Growth and productivity rates have been slower, and unemployment levels higher. As the proceeds of growth have been very unequally divided, the wealth gap has soared, without the promised pay-off of wider economic progress. Financial crises have become more frequent and more damaging in their consequences.

The record on growth and unemployment

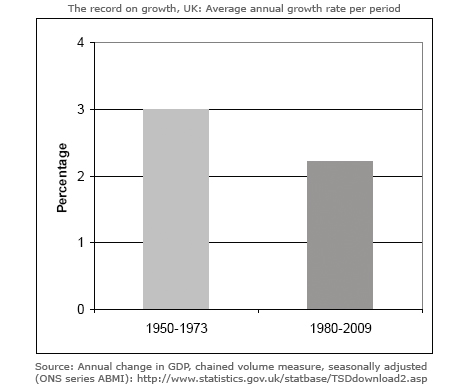

We start with the record on growth. Figure 1 for the UK shows an average annual growth rate of 3 per cent from 1950 to 1973. The figures are low by international comparisons – Germany, Japan and France all did better – but high by historic ones. Since 1980, in contrast, the growth rate has fallen to an average of 2.2 per cent a year.

This fall in the growth rate has been a global phenomenon. At 3.2 per cent, the annual rate of real world growth was significantly lower from 1980 to 2009 than the 4.8 per cent from 1950 to 1973. This pattern holds for all the major economies. The US, UK, Japan, Germany and France all experienced slower growth after 1980 than during the post-war era.

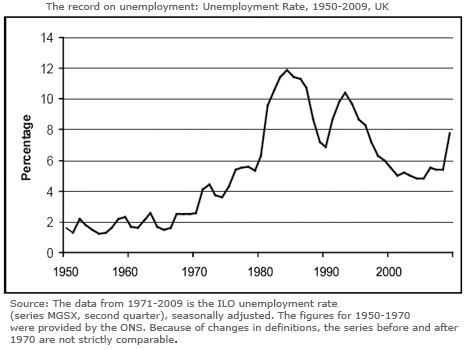

Partly as a result of this slowing growth rate, the British economy, along with most high income economies, has been run at a much higher level of unemployment. In the two immediate post-war decades, the problem of the mass unemployment of the 1930s had been largely cracked. In the era of “managed capitalism” from 1950 to 1973, as shown in figure 2, the UK unemployment rate averaged 1.6 per cent. This was perhaps the nearest the country has come to full employment, at least in the case of males.

Unemployment under “market capitalism” has been much higher. It has averaged 7.8 per cent, nearly five times that of the earlier period. This is despite a steady fall in the share of national output accruing to wage-earners, from around 60 per cent at the end of the 1970s to 53 per cent by 2008. Yet, according to the market theorists, a declining wage share would be an important source of job creation.

As unemployment has soared, it has also become increasingly concentrated, hitting some areas, regions and individuals much more heavily than others. As a result, the jobless are typically out of work for longer than in the past. In the UK the proportion unemployed for more than a year in the period since 2000 has been nearly three times the level of the 1950s. At the end of 2010, it stood at close to 30 per cent.

Of course, “the golden age” of the post-war era with its high growth rates was aided by several factors in addition to the introduction of managed markets and Keynesian fine-tuning, notably the programmes of post-war re-construction and a rapid period of technical change. Nevertheless, controlled markets, capital controls, a stable international monetary system and steadily rising demand were important factors driving success. The period was, above all, evidence of how managed economies, with a mix of national and global controls over markets and the free flow of capital, can be highly successful.

The record on productivity

One of the most important measures of changing dynamism is what has happened to labour productivity – the growth of output per job. “Productivity isn’t everything”, according to the American Nobel Economics Laureate, Paul Krugman, “but in the long run it’s almost everything”. And it is the poor record on productivity that lies behind the slowing growth rates of the last thirty years.

The architects of deregulation claimed that liberated product and labour markets would unleash a new spirit of enterprise, and close the UK’s gap in productivity with the US and leading European nations. Yet the evidence is that freer markets, hands-off government and soaring corporate pay at the top have failed to engineer a significant improvement in Britain’s productivity and innovation record.

In some ways Britain is more entrepreneurial. Business schools are booming and entrepreneurial aspirations have grown. Yet these aspirations have yet to be translated into a noticeable improvement in the quality of entrepreneurship. New business-start up rates have marginally improved and there has been a steady rise in the number of small businesses. But the rate of business failure has remained pretty static in recent years while the UK had fallen from seventh in the world competitiveness rankings (compiled by the World Economic Forum) in 1997 to thirteenth in 2009.

Although productivity rates improved sharply in the 1980s in parts of manufacturing, this was largely because of the mass shedding of jobs at the time. Privatisation of state owned firms also led to improved productivity in several industries, such as steel, which lost close to half its workforce.

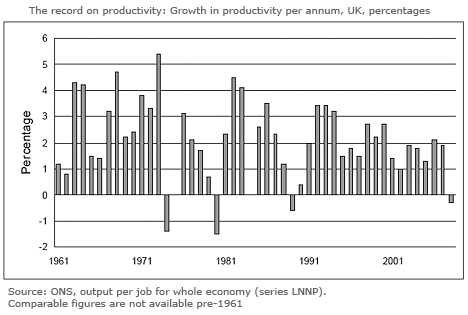

Overall, however, as shown in figure 3, productivity growth has deteriorated since 1980, averaging 1.9 per cent a year to 2008, compared with an annual average rise of 2.95 per cent from 1961 to 1973.

The slipping in the productivity rate during the 1970s and 1980s can perhaps be explained away by the economic difficulties of the 1970s and a delayed reaction to the impact of the dramatic switches in direction – deflation, privatisation and deregulation – of the 1980s. What is less easily explained by the new orthodoxy is why there was not an improved performance after 1990 from the freeing up of markets and lower inflation.

Despite leading the pack of rich nations when it came to de-regulation, the US also displayed a poor record from 1990. The country enjoyed a boost to productivity in the years of the late 1990s to the early 2000s – when it reached 2.5 per cent a year – a success which came to be viewed at the time as a justification for the opening up of markets. Nevertheless, the longer performance from 1990 cannot be described as outstanding. Productivity rose by an annual average of 1.9 per cent in the fourteen years to 2004, compared with just over 3 per cent from 1960 to 1973.

Internationally, the UK has slightly closed the productivity gap with its main international competitors over the last two decades, but it still lags well behind the US, Germany and France. According to a study by the Economic and Social Research Council, the reasons include “a relative failure to invest, failure to innovate, poor labour relations, trade distortions attributable to Empire, antagonism towards manufacturing, ‘short-termism’ among business leaders and financial institutions, technological backwardness and lack of entrepreneurship”.

Britain’s weak record on productivity is in part due to the failure to translate the rising profit share that has occurred since the 1980s into productive investment. Because of the low level of investment, Britain’s infrastructure remains poor compared with its main competitors. Too many plants operate with antiquated systems, while levels of training have lagged behind other countries. Despite the introduction of freer markets, funding for training, research and development and innovation has slowed. Manufacturing entrepreneurs like James Dyson who invest in engineers are the exception.

The evidence is of a strong link between R&D and related capital spending and added value, and eventually profitability. Yet, apart from a handful of industries such as defence, pharmaceuticals and mobile phones, UK companies invest less in R&D, innovation and capital equipment than their international competitors. In most industries the levels of capital expenditure by foreign companies in Britain greatly exceed that of indigenous companies. In the 1960s and 1970s, the UK’s spending on R&D as a share of GDP was comparable to its leading competitors. Since then, the UK has slipped badly behind, and in 2005 spent a lower proportion than in 1973. In contrast, most leading economic nations increased their share of GDP spent on R&D. As one former leading industrialist has complained “The British tragedy is that we have moved from a system of high R&D spend, accompanied by rotten management, to one of low R&D spend, accompanied by a different form of poor management!”.

Boom and bust

A fourth test relates to economic volatility. One of the central tenets of the free market theorists was that markets would deliver greater stability. The Chicago-based Robert Lucas, one of the most influential of the new thinkers, with his “rational expectations” theory of boom and bust, demonstrated that, with rational individuals, perfect capital markets and full information – assumptions at the heart of economic theory – governments would be irrelevant to the delivering of economic stability. In 2003, Lucas, who won the Nobel Prize for Economics in 1995, gave the Presidential Address at the annual meeting of the American Economic Association. “The central problem of depression-prevention”, he momentously explained to his audience, “has been solved, for all practical purposes”.

By this he did not mean that the economic cycle had disappeared, or that the economy would not suffer occasional setbacks, just that the days of severe recession were over, and that economic fine-tuning was of no value. A year later, in February 2004, Ben Bernanke, a former Princeton Professor and soon to be appointed Chairman of the Federal Reserve, gave a speech called “The Great Moderation”, which made a similar point. Bernanke claimed that because of the apparent decline in the variability of both output and inflation from the late-1980s, modern macroeconomics had moderated the problem of the business cycle. According to these accounts, from two of the leading economic theorists in the US, the disaster of 2008-2009 should not have happened.

Despite the theorists’ critique of the role of state intervention, active intervention to moderate the business cycle had a strong track record in the post-war era. As the American economist Hyman Minsky observed in 1982, “The most significant economic event of the era since World War II is something that has not happened: there has not been a deep and long-lasting depression”. Despite claims that the injection of market forces would reduce the capitalist tendency towards instability, the world became a more turbulent place in the next three decades than in the immediate post-war period.

The IMF has generally been reluctant to use the word recession, but when forced, its chief economists have defined a “global recession” informally as a year with a global growth average of less than 3 per cent. This is because while 3 per cent would be a strong rate for rich countries, emerging market economies have much higher “normal” growth rates. In these countries a fall in growth to below a figure of 3 to 4 per cent is similar in impact to negative growth in rich economies.

On this definition, the world has experienced no less than five recessions since 1980. Moreover, the busts have been getting steadily larger. In contrast, as shown by Robert Skidelsky, political economist and biographer of Keynes, there were no global recessions in the era of managed capitalism – the world did not record a single year from 1950-1973 when growth fell below 3 per cent.

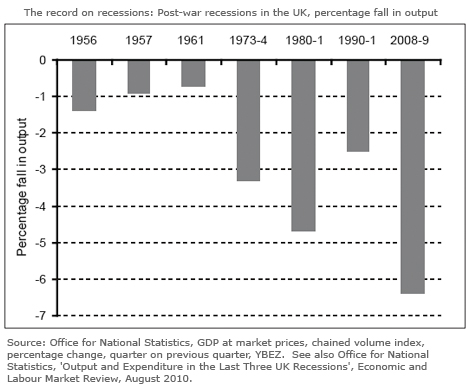

On the alternative, more conventional definition of a recession – negative real growth in two successive quarters – this pattern still holds. There have been more and deeper recessions since 1980 than between 1950 and 1973. Take the UK economy. Although it experienced a number of exchange rate and stop-go crises in the two decades from 1950, there were only three shallow and short-lived recessions in this period. As shown in figure 4, there was one in 1956, when output fell by 1.4 per cent over three quarters; one in 1957, when output fell by 0.9 per cent over two quarters; and then one in 1961, when it fell by 0.7 per cent over two quarters.

In contrast, the period since 1980 has been distinguished by more frequent, more prolonged and more severe economic shocks than the earlier period, with three deep-seated recessions. Specifically, in 1980-1981 when output fell by 4.7 per cent (over five quarters); 1990-1991, when it fell by 2.5 per cent (over five quarters); and 2008-2009 when it fell by 6.4 per cent (over six quarters).

Not only have the UK and the world experienced more and deeper recessions; the crises of recent times have had very different origins. Earlier post-war dips (mild as they were by comparison) were triggered by deflationary policies that were needed to get inflation under control (as was that of 1980-1982). The most recent recessions have had nothing to do with inflation (or soaring wage demands). They have had much more to do with rising asset prices, driven by excess profits and unsustainable credit, and fuelled by financial deregulation.

This has also been the main cause of the upsurge in financial crises, most of them associated with a torrent of currency, stock or property speculation. In the two decades from 1950 there were no banking crises and relatively few financial crises. Since the end of the 1970s, the number of such crises has mushroomed. As Financial Times columnist Martin Wolf has put it, “financial liberalisation and financial crises go together like a horse and carriage”.

From the beginning of the 1980s, the number of banking failures in the US started rising sharply, a problem exacerbated by the impact of bank deregulation. In October 1987, the world’s leading stock markets crashed, their largest fall in a day since the crash of 1929. A serious fall-out for the world economy was only averted by a huge injection of global liquidity. In 1989, the bursting of a serious property bubble in Japan, triggered by a series of bank liquidity crises, led to a decade-long period of deflation and a sustained collapse in Japanese shares prices. It had been preceded by a decade of rising profits (which had risen to 40 per cent of output) and soaring assert prices. Between 1990 and 1992, Norway, Sweden and Finland all suffered a banking crisis sparked by a similar property boom, deregulation of financial services, and excessive lending by banks. Again, only decisive action by the national governments prevented a more prolonged fall-out.

Five years later, the Asian currency crisis, driven by financial over-reach, caused mayhem across south-east Asia when currency speculators pulled billions out of Asian currency markets. In 2000, the collapse of the dot.com bubble brought world stock markets crashing once again.

As the age of stability gave way to the age of turbulence, the chronic economic crisis that hit the global economy in 2008 provided the ultimate test of the effectiveness of the near thirty-year long experiment in market capitalism. It was a test that resulted in dramatic failure. Yet, according to the market theorists, the economic meltdown of 2008-2009 should not have happened. The promise of selfregulating markets might have worked in the computerised mathematical models of the neoliberal economic theorists, but they failed in the real world.

Even on the basis of its own goals, the economic strategy of the last thirty years can claim only one success, the taming of inflation. On all other goals, it has failed. Instead, the most marked legacy of the market experiment has been a persistent rise in inequality, one so sharp that it has sent the wealth and income gap in the United Kingdom and the United States back to levels last seen in the inter-war years. Far from being a mechanism for delivering economic success, the primary function of the Anglo-Saxon economic model, it seems, has been to hand power to a new generation of business executives and financiers who have used it to enrich themselves, irrespective of the consequences for the economy and the workforce.

This is a view no longer confined to critics of the market. In an article in the Daily Telegraph (22.7.11), entitled “I’m Starting to think the Left Might be Right After All”, Charles Moore, the former editor of the paper, examined whether “what the Right calls ‘the free market’ is actually a set-up”. His conclusion:

It turns out … that a system purporting to advance the many has been perverted in order to enrich the few. The global banking system is an adventure playground for the participants, complete with spongy, health-and-safety approved flooring so that they bounce when they fall off. The role of the rest of us is simply to pay.

Yet, despite its record, and the growing list of sceptics, the market orthodoxy remains largely intact. The overwhelming virtues of markets are still being taught in business schools and economic departments. State industrial policy that could provide the means to hasten economic recovery is shunned. The Treasury remains little more than an outpost of the City, while the Coalition government believes that the solution to Britain’s fragile economy lies in another boost of market freedom, with further restrictions on workplace rights. The lesson of the last thirty years, spelt out so clearly by Charles Moore, that what the British economy needs is a greatly reformed model of capitalism, seems yet to have been learned.